US demand for cups & lids to reach $10 billion

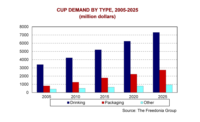

Demand for cups and lids in the US is projected to expand 4.4% per year to $10.0 billion in 2018, driven by above average gains for food packaging cups and an improved outlook for foodservice revenue growth relative to its 2008-2013 performance. According to analyst Esther Palevsky, “Demand will be propelled by the important role of beverages as revenue generators for restaurants and a growing focus on specialty beverages among foodservice operators.” These factors will drive growth for higher value cup and lid products, such as paper hot cups, polyethylene terephthalate (PET) cups, and specialty lids. Prospects for costlier types of cups will be strengthened by the growing number of cities enacting bans or restrictions on foamed polystyrene disposables and by restaurant chains transitioning away from foam cups as part of corporate sustainability initiatives. Foodservice, which accounted for two-thirds of demand in 2013, will remain the dominant cup and lid market. These and other trends are presented in Cups & Lids, a new study from The Freedonia Group, Inc. (freedoniagroup.com), a Cleveland-based market research firm.

Among cup types, the fastest gains are anticipated in the packaging cup segment due to favorable consumption trends in a number of applications, along with the convenience, portability, and portion control benefits of single serving cup packaging. Paper cups will experience the fastest growth among drinking cup types, a shift in the competitive landscape. Advances will reflect environmental concerns about foam cups, growing restrictions on polystyrene foam products, pressure from environmental groups, and conversions to paper from foam by high volume foodservice providers. Foam cup demand will also be threatened by the commercialization of recyclable plastic cups with insulation properties comparable to those of foam.

Lid demand growth will outpace that for cups, rising 4.7% per year to $1.3 billion in 2018. Advances will be fueled by expanding carryout food and beverage sales from restaurants and retail stores, an increasing percentage of drinking cups utilizing lids, heightened demand for costlier specialty lids, and healthy increases for single serving packaging cups, all of which have some type of lid.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!