Declining demand in a number of national markets, principally France and Italy, and the continuing lack of significant inflationary pressures, are the main factors behind growth in Europe’s flexible packaging market slowing to 1.3 percent in both value and volume terms in 2013, down from 2.1 percent and 1.8 percent respectively in 2012.

Declining demand in a number of national markets, principally France and Italy, and the continuing lack of significant inflationary pressures, are the main factors behind growth in Europe’s flexible packaging market slowing to 1.3 percent in both value and volume terms in 2013, down from 2.1 percent and 1.8 percent respectively in 2012.

This is one of the main conclusions from PCI’s latest annual report on the $16.6 billion European converted flexible packaging market with growth expected to pick up only slightly in 2014. Report author Paul Gaster, also notes, "The growth slowdown reflects the fact that a number of economies in the Eurozone are still struggling with the effects of recession, which has reduced demand for packaged foods in these countries."

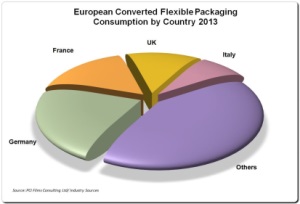

As in previous years, there were some significant regional and national differences in value and volume demand trends. Sales in Germany, Europe’s largest flexible packaging market, continued to see some modest growth, as to a lesser extent did the UK. However, demand in Italy, Greece and Portugal continued to contract, with negative growth seen in France for the first time since 2009. Demand was most buoyant in some emerging markets in Eastern Europe, notably Russia and Poland, which grew at over four times the European average. Sales growth in Turkey, a major emerging market, while still strong relative to the European average, fell back compared with the previous year.

Compared with the metal can, glass and paperboard packaging industries, Europe’s flexible packaging industry continues to be highly fragmented with the top 20 players accounting for around 70 percent of the market. However, ongoing consolidation continues to be steadily changing the structure of the industry, mostly with the backing of private equity finance. Major developments include the emergence of Sun Capital portfolio business Coveris as a top 10 player, and the rapid growth via acquisition of Schur Flexibles. Approaching 20 percent of the industry’s sales in Europe is currently generated by private equity portfolio companies.

Now in its 14th edition, PCI Films Consulting’s ‘The European Flexible Packaging Market’ has become an invaluable tool in driving business planning, investment and future product developments. Based on original field research, it is the most recent and comprehensive report available on the European market, providing over 400 pages of historical data and highly detailed market analysis and statistics for 2013, estimates for 2014 and forecasts through to 2018.

PCI Films Consulting Ltd.

+44 (0) 1604 749001

Declining demand in a number of national markets, principally France and Italy, and the continuing lack of significant inflationary pressures, are the main factors behind growth in Europe’s flexible packaging market slowing to 1.3 percent in both value and volume terms in 2013, down from 2.1 percent and 1.8 percent respectively in 2012.

This is one of the main conclusions from PCI’s latest annual report on the $16.6 billion European converted flexible packaging market with growth expected to pick up only slightly in 2014. Report author Paul Gaster, also notes, "The growth slowdown reflects the fact that a number of economies in the Eurozone are still struggling with the effects of recession, which has reduced demand for packaged foods in these countries."

As in previous years, there were some significant regional and national differences in value and volume demand trends. Sales in Germany, Europe’s largest flexible packaging market, continued to see some modest growth, as to a lesser extent did the UK. However, demand in Italy, Greece and Portugal continued to contract, with negative growth seen in France for the first time since 2009. Demand was most buoyant in some emerging markets in Eastern Europe, notably Russia and Poland, which grew at over four times the European average. Sales growth in Turkey, a major emerging market, while still strong relative to the European average, fell back compared with the previous year.

Compared with the metal can, glass and paperboard packaging industries, Europe’s flexible packaging industry continues to be highly fragmented with the top 20 players accounting for around 70 percent of the market. However, ongoing consolidation continues to be steadily changing the structure of the industry, mostly with the backing of private equity finance. Major developments include the emergence of Sun Capital portfolio business Coveris as a top 10 player, and the rapid growth via acquisition of Schur Flexibles. Approaching 20 percent of the industry’s sales in Europe is currently generated by private equity portfolio companies.

Now in its 14th edition, PCI Films Consulting’s ‘The European Flexible Packaging Market’ has become an invaluable tool in driving business planning, investment and future product developments. Based on original field research, it is the most recent and comprehensive report available on the European market, providing over 400 pages of historical data and highly detailed market analysis and statistics for 2013, estimates for 2014 and forecasts through to 2018.

PCI Films Consulting Ltd.

+44 (0) 1604 749001