Two Out of Three Stand-up Pouches Used in Pet Foods and Beverages

-Report By PCI Films Consulting

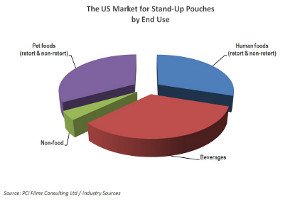

The US stand-up pouch market has seen dramatic growth over the past five years, increasing by 50 percent in unit volume terms to approaching 17 billion units in 2013. Beverages and pet food are the largest end use categories, each accounting for one-third of demand, closely followed by human food applications with around 30% share.

Stimulating the recent growth in pouches has been the drive to replace plastic and glass bottles and cans, packaging cost reduction and consumer convenience. In its new report on the stand-up pouch market, PCI Films Consulting forecasts that US demand for pouches will continue to grow by around 7% p.a. to reach nearly 24 billion units in 2018, at least twice as fast as volume growth expected in the US flexible packaging market as a whole.

Report author Julian Lozowick, comments: “The most significant increases in volume have come only in the last two years, particularly in liquid products within the human foods non-retort category, such as in the packing of baby foods and fruit compote and purees. The use of pouches for dry food products in general has been growing more steadily, but even here some categories have seen rapid recent growth.” Future increases in volume are expected to come from a wide variety of end uses - frozen foods and fruit compotes, frozen spirits, cocktails, baby food, shredded and diced cheese, laundry and dishwashing refill packs and soups. Other opportunities are only in the early stages of development but pouches used to pack motor oils, dietary meal solutions and possibly olive oil and fresh vegetables are forecast to grow in volume.

The growing interest in pouches has been satisfied on the supply-side by the expanding infrastructure of toll converters and contract packers as well as advances in pack resealability and slider technologies. Pre-made pouches retain a majority share of the US stand-up pouch market with printed laminate for form-fill-seal applications currently accounting for less than a quarter of total pouch units.

PCI’s comprehensive new report, ‘The US Market for Stand-up Pouches to 2018’, which follows publication earlier this year of a similar study on the European market, analyses the major factors driving growth in this dynamic market. Based on extensive fieldwork, the report provides details of the current US stand-up pouch market by unit volume; area of substrates used (M²) and value; existing and planned new filling capacities; trends in more than 30 end-use sub-sectors; usage split between pre-made and form-fill-seal formats; and profiles of the leading pouch suppliers. With forecasts to 2018, this market-leading report provides valuable strategic insights into how the US stand-up pouch market is expected to develop over the next five years.

For more details on this report, click here.

-Report By PCI Films Consulting

The US stand-up pouch market has seen dramatic growth over the past five years, increasing by 50 percent in unit volume terms to approaching 17 billion units in 2013. Beverages and pet food are the largest end use categories, each accounting for one-third of demand, closely followed by human food applications with around 30% share.

Stimulating the recent growth in pouches has been the drive to replace plastic and glass bottles and cans, packaging cost reduction and consumer convenience. In its new report on the stand-up pouch market, PCI Films Consulting forecasts that US demand for pouches will continue to grow by around 7% p.a. to reach nearly 24 billion units in 2018, at least twice as fast as volume growth expected in the US flexible packaging market as a whole.

Report author Julian Lozowick, comments: “The most significant increases in volume have come only in the last two years, particularly in liquid products within the human foods non-retort category, such as in the packing of baby foods and fruit compote and purees. The use of pouches for dry food products in general has been growing more steadily, but even here some categories have seen rapid recent growth.” Future increases in volume are expected to come from a wide variety of end uses - frozen foods and fruit compotes, frozen spirits, cocktails, baby food, shredded and diced cheese, laundry and dishwashing refill packs and soups. Other opportunities are only in the early stages of development but pouches used to pack motor oils, dietary meal solutions and possibly olive oil and fresh vegetables are forecast to grow in volume.

The growing interest in pouches has been satisfied on the supply-side by the expanding infrastructure of toll converters and contract packers as well as advances in pack resealability and slider technologies. Pre-made pouches retain a majority share of the US stand-up pouch market with printed laminate for form-fill-seal applications currently accounting for less than a quarter of total pouch units.

PCI’s comprehensive new report, ‘The US Market for Stand-up Pouches to 2018’, which follows publication earlier this year of a similar study on the European market, analyses the major factors driving growth in this dynamic market. Based on extensive fieldwork, the report provides details of the current US stand-up pouch market by unit volume; area of substrates used (M²) and value; existing and planned new filling capacities; trends in more than 30 end-use sub-sectors; usage split between pre-made and form-fill-seal formats; and profiles of the leading pouch suppliers. With forecasts to 2018, this market-leading report provides valuable strategic insights into how the US stand-up pouch market is expected to develop over the next five years.

For more details on this report, click here.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!